Blog

Thursday

8

MAY

2025

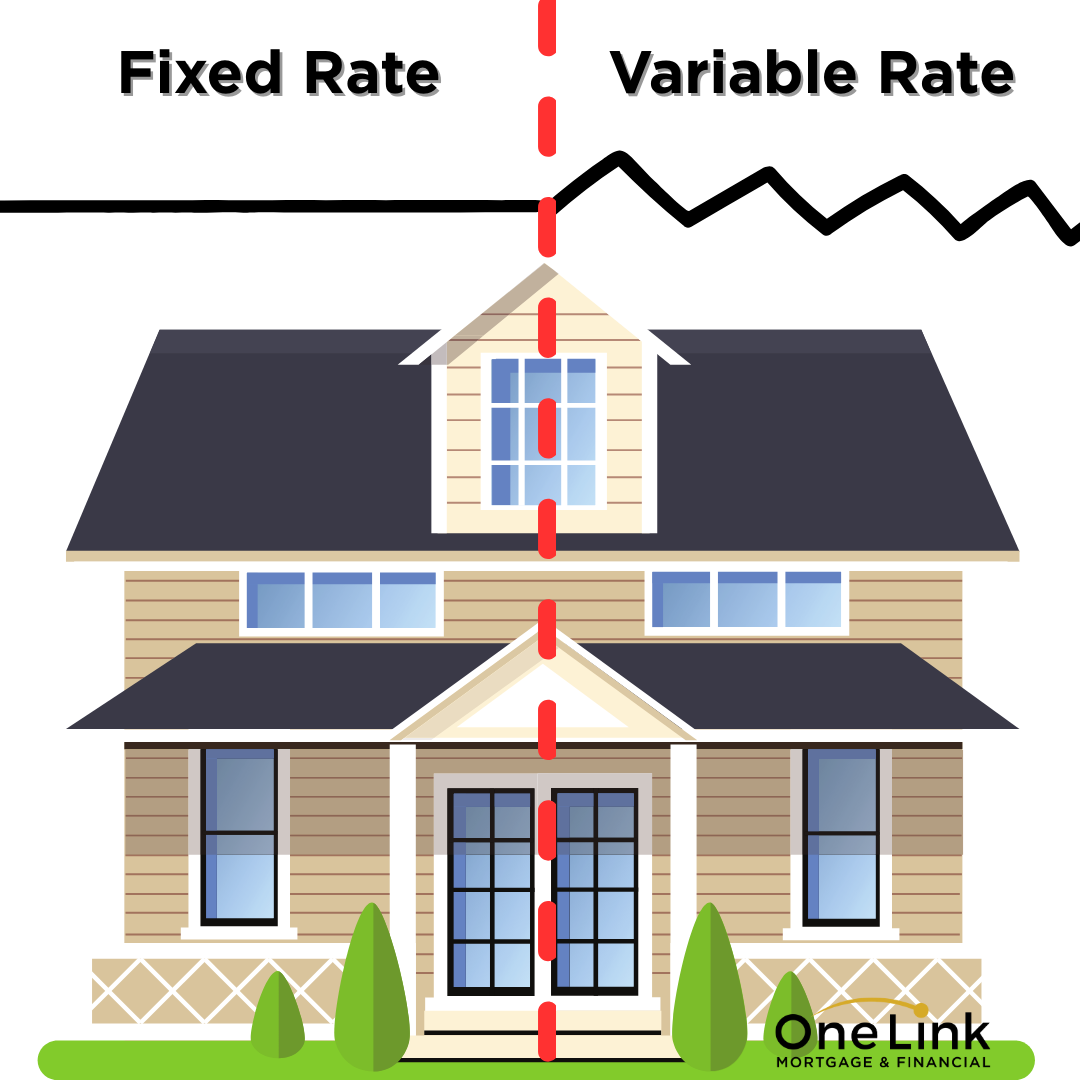

Why Is the Difference Between Fixed and Variable Mortgage Rates So Confusing?

If you're shopping for a mortgage in Manitoba, you've likely

come across the choice between fixed and variable rates. While it may seem

straightforward, the factors influencing these rates can be quite complex.

Understanding what causes them to rise and fall can help you make an informed

decision about your mortgage.

What Affects Fixed Mortgage Rates?

Fixed mortgage rates are primarily influenced by the bond

market. Lenders set fixed rates based on the yields of Government of Canada

bonds. When bond yields rise, fixed mortgage rates tend to increase, and when

bond yields fall, fixed rates typically decrease. Factors that influence bond

yields include:

- Inflation:

Higher inflation generally leads to higher bond yields and, in turn,

higher fixed mortgage rates.

- Bank

of Canada’s Policies: When the central bank raises or lowers its

benchmark interest rate, it can indirectly impact bond yields.

- Economic

Conditions: Strong economic growth can push bond yields higher,

leading to increased fixed mortgage rates.

What Affects Variable Mortgage Rates?

Variable mortgage rates are tied to the Prime Rate, which is

influenced by the Bank of Canada's overnight lending rate. However, it’s

important to note that Prime Rate is not the same as your lender’s variable

mortgage rate—lenders apply a discount or premium on the Prime Rate to

determine your final variable rate.

Key factors affecting the Prime Rate include:

- Bank

of Canada’s Policy Rate: When the Bank of Canada raises or lowers its

policy rate, the Prime Rate usually follows suit.

- Economic

Growth: A strong economy may lead to higher rates to control

inflation, while weaker economic conditions may result in rate cuts.

- Inflation

Trends: If inflation is rising too quickly, the Bank of Canada may

increase rates to slow spending and borrowing.

Why the Confusion?

Many borrowers assume that variable rates are always lower

than fixed rates, but this isn't always the case. Economic shifts, government

policies, and global events can cause rates to fluctuate unpredictably.

Additionally, since lenders apply different discounts or premiums to the Prime

Rate, variable mortgage rates can vary from one lender to another.

Note about Mortgage Renewals

When renewing your mortgage, it's crucial to explore your

options at least 30 days before your renewal date to secure the best

fixed or variable rate. We can lock in mortgage rates for up to 120 days,

protecting you from potential rate increases while allowing flexibility—if

rates drop, we can often negotiate a lower rate with the lender. Planning ahead

ensures you get the most competitive mortgage renewal terms, whether you prefer

the stability of a fixed rate or the potential savings of a variable rate.

If you’re unsure whether a fixed or variable rate is right

for you, speaking with a trusted One Link Mortgage Broker can help. We can

analyze your financial situation and risk tolerance to find the best mortgage

option tailored to your needs.

Looking for expert mortgage advice in Manitoba? Contact One

Link today to explore your options and secure the best rate for your home

financing! 204-954-7620 or save@onelinkmortgage.com

LATEST POST

- Why Is the Difference Between Fixed and Variable Mortgage Rates So Confusing?

- First-Time Home Buyer Budgeting in Manitoba: What to Expect on a $350,000 Purchase

- Manitoba Housing Market Outlook 2025: What Buyers and Homeowners Need to Know

- Spring Homebuying Season in Manitoba: Get Pre-Approved and Find Your Dream Home